How COVID Changed Shopping This Year

This year many retailers are swapping in-store Black Friday deals for an entire month of online deals with Cyber-November, so it's mid-November and we already find ourselves well into the holiday shopping season. With that said, it seems like an appropriate time to look at shopping trends during COVID, changing shopping behaviors that may stick post-COVID, and what that means for your holiday marketing strategy.

While I sound like a broken record, recency is everything. Lucky for us, YouGov has been tracking how the pandemic is impacting consumer sentiment, media usage, eating patterns, shopping habits, and more. Our COVID questions are integrated into our continuous interviewing for YouGov Profiles and the daily brand health data in YouGov BrandIndex helps you understand consumers' evolving relationships with brands.

Here are some key takeaways on changes in shopping behavior to inform and inspire as you navigate holiday and finalize your plans for 2021.

We're Spending Less In-Store (Except Groceries)

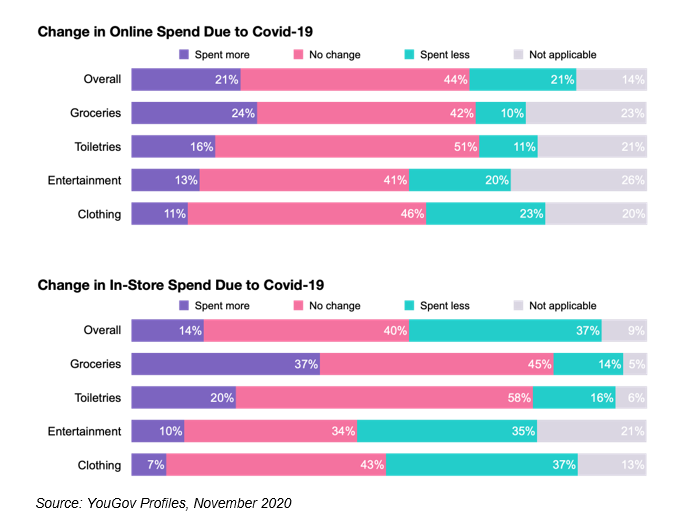

One in five Americans is spending more online and one in three is spending less in-store as a result of COVID-19. As we spend more time at home, we're spending more money on groceries & toiletries, both online and in-store. On the flip side, we're spending less on entertainment and clothing, online and especially in-store.

Gen Z is spending more online on clothing (19%) and entertainment (23%), whereas the increase in online spend for other generations is driven mostly by buying groceries online. With bigger households and kids spending more time at home too, parents of kids under 18 are more likely to have increased spend on groceries for online (31%) and in-store (46%).

People who increased their online spend are less optimistic about the pandemic (51% think the COVID situation in the US is getting worse vs 43% overall) and are less comfortable going into most types of public places (i.e., stores, restaurants, mass transit, etc.). These consumers will likely take longer to return to shopping in-store and their online shopping behaviors may become ingrained in the meantime.

We're Filling Our Time Instead of Our Closet

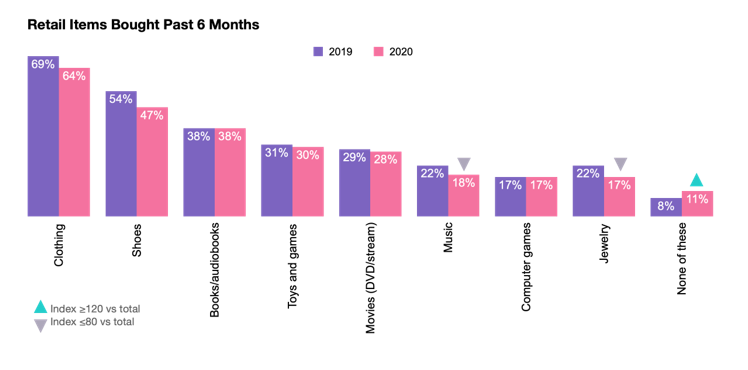

COVID has brought a new twist on the purchasing "experiences over things" trend. Purchasing of books, toys, movies, and games is holding as we look for ways to entertain ourselves and fill our time at home. But we see drops in people buying clothes, shoes, and jewelry -- a trend that might not reverse until life outside the home fully reopens. This will have huge implications for many retailers during the holidays and moving into Q1. As an example, should boost strategies change? Should you move to a different discounting strategy? Should you offer different discounts for pick up vs. online? Is there varied messaging based on COVID needs vs. holiday needs?

We see declines in purchasing of all types of clothing and shoes -- except sweatshirts and yoga pants/leggings (the new work from home uniform!?!). Work & special occasion clothing such as suits, dresses, pumps, are down the most dramatically. All types of jewelry are down year over year, although engagement rings see the smallest decline (-7%).

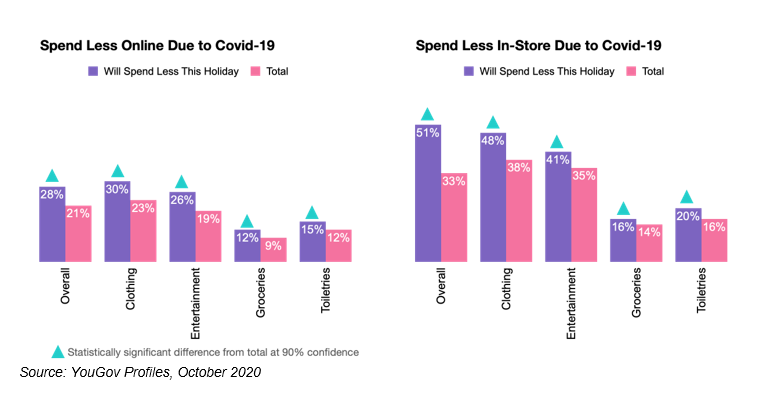

In terms of how this will play out over the holiday, nearly one-third of Americans plan to spend less this holiday season than last year -- that's about 78 million people. These consumers are more likely to have suffered reduced hours or a furlough at work, and they skew female, age 50-64, and suburban. They have made deeper cuts to their spending, especially on clothing in-store.

We're Starting To Become Online-Only

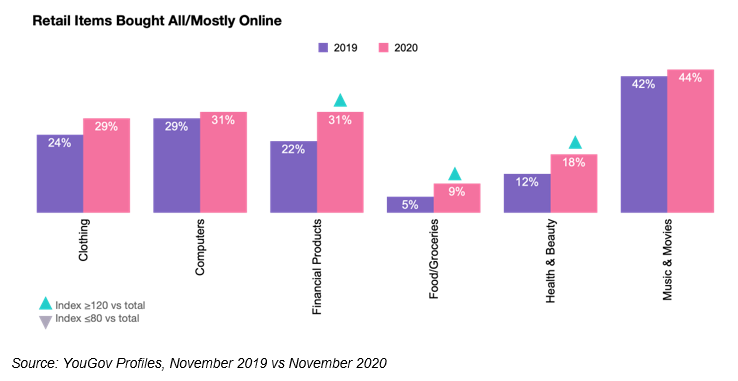

While the majority of people continue to shop a combination of online and in-store, we're seeing notable growth in the number of people saying they shop exclusively or predominantly online for many categories. Upwards of three in ten consumers say they buy online for all/most of their clothing, computers, financial products, and music & movies.

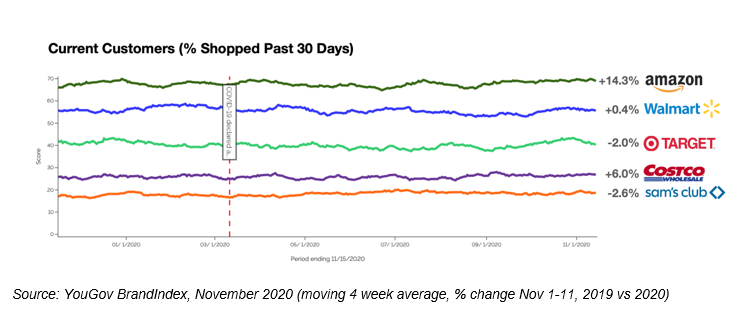

As spending online increases, Amazon is reaping the lion's share of those gains with +14.3% year-over-year growth in people shopping the retailer. We also see growth for Costco (+6.0 vs last year), as consumers look to stock-up and reduce their frequency of shopping trips.

Department Stores, which were already struggling, have been especially hard hit by the declines in spend on clothing and decrease in in-store shopping. Current customers are down year-over-year for Macy's (-31%), Kohl's (-25%), and JCPenney (-23%). We're seeing similar declines for browsing-driven discounts stores TJ Maxx (-22%) and Marshall's (-22%). Talk about an opportunity to transform your holiday strategy! These brands should be looking to lean into needs of the changing COVID-consumer/media landscape and messaging that would make them a more attractive buy vs. Amazon or big box. Time to defend their market share!

As marketers, questions to ask ourselves include: What is my Amazon strategy? Am I making it easy for shoppers to stock up on my products...wherever they prefer to shop? What opportunities am I creating for shoppers to discover my brand & products if they shop exclusively online? Do I have an Amazon storefront? Do I make Instagram shoppable? Can consumers pay via PayPal, Apple Wallet, After Pay, Venmo, etc.?

Some of the realities of how we shop now will revert when we fully re-open, but some are accelerations of trends that were already in play. It's my POV that we will not take steps back but lean into the ease of this change, permanently. Being easily purchasable online -- and discoverable online -- must be central in both your short-term but long-term strategy.

It's a challenging time for many categories, but up-to-date data is available and helps a lot. The right knowledge partner can help you go forth into the new year with confidence. Contact me if you're interested in seeing this data, and more, broken out for your specific target audiences, brands, etc. I'm here to strategize and help. Send your request here.

Photo courtesy of Tamara Alesi.

Click the social buttons to share this story with colleagues and friends.

The opinions expressed here are the author's views and do not necessarily represent the views of MediaVillage.com/MyersBizNet.

Tamara Alesi

How can we do it better? What can we do different and smart? Tam’s confidence and conviction inspire colleagues and partners alike to find more collaborative and innovative ways to connect with customers and embrace solutions, delivering real-world res…