RESEARCH: Where Advertisers and Media Agencies Agree and Disagree on Priorities

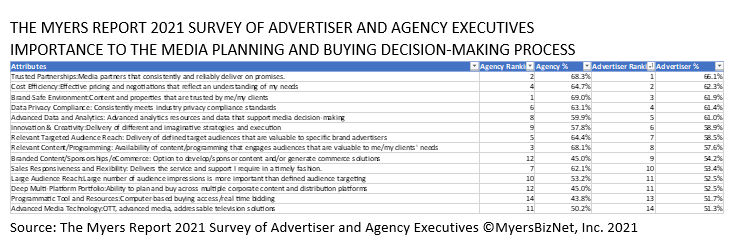

The Myers Report 2021 Survey of Advertiser and Agency Executives confirmed overall advertiser/agency alignment, uncovered several surprises, and suggests some agency priorities are less important to their clients. The study conducted online earlier this year among 464 agency and 236 advertiser professionals, suggests that media company investments are not always in sync with the priorities of their clients -- both agency and advertiser. Respondents were asked to rank the importance of each attribute to their media decision-making process (0-10 with 10 = most important, 0 = not at all important). Results are based on the percent of respondents rating each attribute on a score of 8, 9, 10 (top 3 box)

- Trusted partnerships and brand safe environment remain critical influences in the media allocation consideration, but both have declined over the past three years from low 80% top 3-box (on a 10-point scale) ratings to the 60% range.

- Cost efficiency is slightly more important to advertisers than agencies, a reversal from past studies (reflecting the increased representation of procurement officers among survey respondents).

- Data privacy concerns have emerged as an important reality being confronted by executives across the media, advertising and marketing ecosystem.

- Deep multi-platform portfolios, programmatic tools and resources, and advanced media technologies such as addressable and OTT, while competitively important, do not yet appear to be impacting significantly on the media decision-making process.

- Similarly, large audience reach is less of a priority than many media sellers believe, and targeted/relevant audience reach has declined significantly from #1 most important priority in 2019 and 2020 to #5 among agencies and #7 among advertisers. The restructuring of decision-making at advertisers from brand marketers to procurement and in-house agencies, and at agencies to younger data-focused analysts is a primary force behind this reallocation of priorities.

- The "Branded Content and Sponsorships" category has increased in value from 35% to 54%, attributable to the addition of "e-commerce", reflecting the emergence of commerce as a growing priority as Amazon, Walmart, Target and several other retailers launch media sales organizations and focus on direct-to-client selling.

- Not surprisingly, responsive and flexible sales organizations are more important to agency respondents.

Over the next several weeks, MediaVillage will be sharing insights from its 2021 Survey of Advertiser and Agency Executives and from the 2021 Media Brand Equity Survey of Consumers, Advertisers and Agency Professionals. Proprietary insights are being shared with MediaVillage member companies. To schedule a presentation, contact Maryann@MediaVillage.com.