According to Hulu, Age Is Not a Factor in Digital Fluency

"Digital fluency is more about attitude and behaviors than it is about age," stated Julie DeTraglia, Head of Research, Hulu. Her company just released the results of a major new research study on what constitutes digital fluency, focusing on how consumers adapt different digital journeys throughout different forms of media, in e-commerce and across lifestyle brands. The results confirmed tested truths while also offering some surprising insights, which she recently discussed with MediaVillage.

Charlene Weisler: What were the major takeaways of this new study?

Julie DeTraglia: We found that digital fluency is not driven by age. It was the impact of technology that prompted behavior change. Digital connections are now normal for people, media and brands. We also found that media is core to digital identity because social and streaming are gateways to digital consumption.

Weisler: What were the major surprises?

DeTraglia: The biggest surprise was that across all generations (including Gen Z) just as many people identified themselves as Minimalists and Averse (lower end of spectrum) as they did Maximizers and Creators (higher end of spectrum). We also were surprised and happy to see that social media, streaming video and online transactions are all tightly intertwined when it comes to changing habits.

Weisler: Do the consumer profiles of the younger generations differ along the spectrum? For example, do the Averse have a different demo profile to the Maximizers?

DeTraglia: No, they are demographically similar, which is the point behind the study. Just because people are mapped to a generation doesn't mean they have the same attitudes or perceptions of technology. It ranges more on the behavior than the age.

Weisler: What about the older generations? How do they fall on the digital fluency spectrum?

DeTraglia: Specifically, for Boomers (55+), 2% are Creators, 7% are Maximizers, 15% are Connected, 34% are Confident, 26% are Enlighted, 12% are Minimalists and only 4% are Averse. The biggest difference we saw is that Boomers have a much lower percentage of Creator, Maximizer and Connected identified users and that they are higher in Confident and a lot higher in Enlighted. They over-index in the middle of the spectrum, which is surprising to most.

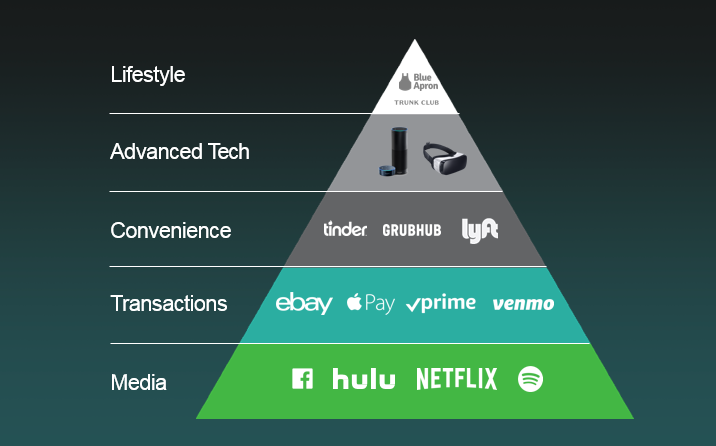

Weisler: Your hierarchy of digital needs looks to be patterned like Maslow's Hierarchy. Can you talk about each hierarchy stage and what it means in the digital journey?

DeTraglia: The hierarchy of digital needs that the user travels along starts with media, which is the foundation to a digital identity and closely related to transactions and shopping. The trend towards connectivity started when Facebook and social media launched, eventually impacting every product of service -- how we communicate, eat, date and transact. Once you're comfortable with media, you slowly move along the journey, you become comfortable with transacting through digital and eventually you begin using applications that make life easier and more convenient like [those centered on] eating, dating, traveling. Advanced technology is the next level, which pushes the consumer to use virtual reality and voice-activated systems that eventually lead to curating a personalized lifestyle and dependence on applications like HelloFresh and Aaptiv and StitchFix, to in turn make your life more convenient.

Weisler: Is it possible to move someone who is more of a technophobe across the digital spectrum?

DeTraglia: Great question. We continue to explore this more at Hulu. It is a large barrier for a consumer who is completely averse to moving along the spectrum. The only wave of movement would be if they were to try something first and realize how much better it will make their lives before they jump in. But we believe it is possible, as some later adaptors of technology are functioning as more connected, which means it is always a possibility.

Weisler: Are there certain consumer categories that attract more Maximizers and Creators (aside from the obvious tech categories)? Any surprises?

DeTraglia: The direct-to-consumer businesses are the ones booming right now which certainly attract Maximizers and Creators. They feel more comfortable to use them and feel like it is a great addition to their lives for the convenience factor. From a Hulu standpoint, we learned that our users are further along the spectrum, so they are more likely to use direct-to-consumer apps and social media. There wasn't anything too surprising here, but we are continuing to explore.

Weisler: What ad messages can be used to reach people by their place in the spectrum? Different messages for the Averse vs Maximizers, for example?

DeTraglia: Marketers and advertisers need to understand that it is more about where they reach these consumers vs. the language used. For example, it is about where the brands capture attention. We know Hulu and other streaming services do that. Consumers at the higher end of the spectrum prefer a different type of ad; they want them to feature people, make the consumer feel like they are a part of the ad, give them a sense of brand personality and take the consumer along a storyline. This came from follow-up work on creative best practices for our advertising partners. These were the aspects -- more immersive commercial experiences that consumers [want] and that video can offer.

Weisler: What are the next steps in this research for Hulu?

DeTraglia: We are a direct-to-consumer business, in this space for a long time, and we know that the people on our service are "empowered" consumers. They are important to us from both a marketing and advertising partnership perspective because they are valuable to reach. We used this data when we designed our new brand campaign, "Better Ruins Everything." We will continue to explore these segments to align with our consumers' needs and expectations. From an advertising partnership perspective, continuing to understand how our consumers are different and what they are more receptive to helps guide our advertisers as to how best to reach and engage their targeted consumers.

Click the social buttons above or below to share this story with your friends and colleagues.

The opinions and points of view expressed in this content are exclusively the views of the author and/or subject(s) and do not necessarily represent the views of MediaVillage.com/MyersBizNet, Inc. management or associated writers.

Charlene Weisler

Charlene Weisler is a media research executive and MediaVillage columnist with experience that spans broadcast, cable, off-platform, non-linear, and broadband. She shares her expertise in set-top box data, SEO, metrics creation, and behavioral psychography i…