Navigating Advertising Through Seismic Shifts in Everything

Nielsen Gauge results for September 2022 show that streaming now accounts for 36.9% of total television usage, up from 35.0% in August. YouTube, counted as part of streaming by Nielsen, is 8.0% of total television usage in that same framework (i.e., 21.7% of the streaming cell). Live viewing is now in the minority, whereas time-shifted, on-demand streaming and other uses of the TV set (videogames for example) are not only collectively in the majority, but growing rapidly. This historic shift from the classical way TV was consumed in the past is happening faster than anyone would have predicted.

In March my column was about the two different modes of entertaining oneself with owned-device-based screen media: longform and shortform. I called them "show mode" vs. "curiosity flow mode" because they are psychologically so different. In "show mode" one decides to make a time investment in watching a story or some sort of other program play out from beginning to end for a half hour, hour, or longer. In "curiosity flow mode" one is able to see something new, see something else new, and keep up the stream of new things to look at as fast as you get tired of the last item.

Neuroscientist Carl Marci years ago stated that the brains of young people have become accustomed to getting a jolt of dopamine and/or oxytocin from seeing something on a screen and then quickly moving on to something else to get that same jolt, which only lasts for the first few seconds of seeing something relatively novel to you.

Nielsen’s Total Audience report shows that the average American adult spends as much time with the web and apps on smartphone and tablet as we spend on television. All of that time on the smaller screens hopping around from bit to bit appears to be rubbing off on how we spend our time with television on all devices. These new media behaviors seem to be pushing us into becoming a short attention span culture, as Neil Postman predicted.

Because advertising-supported streaming services tend to show fewer minutes of ads per hour, the total impression count for television is going down. However, streaming is addressable, and so if brands know how to use addressability and validated research methods, the power of an impression goes up by more than 100%, far more than offsetting the fewer impressions.

We might invent a term here: Television Value Units (TVUs) -- the average percentage of incremental sales produced per impression and across all impressions. There is also DVU for digital, RVU for radio, and so on. TVU is going up as a result of being able to target actual product category purchasers of specific types shown to be responsive to the creative you are currently running. And as a result of being able to take advantage of the added boost of psychologically resonant context. With addressable forms of television and these additional tools the increase in sales effectiveness on average more than doubles while CPMs do not rise as fast. Hence TV, still with the most hours of usage of any medium, is empowered to increase the edge that it always had over all other media types.

Studies by Fox, McKinsey, Bill Harvey Consulting (BHC), Standard Media Index, IRI, Polk and NPD show that YouTube ad investments are correlated with more negative sales results than TV, while YouTube has brought forth other studies showing more positive sales results than TV. As I’ve looked at the latter studies what I note is that they are based on brands that are putting very little into YouTube, and a lot into TV, so that the incremental reach and ROI added by YouTube are real. The problem we (the group above including BHC) saw in our larger data set ($2.2 trillion worth of sales vs. $48 billion in advertising) was that the brands in our study were putting in much larger amounts of YouTube. It’s all a matter of saturation effect. When you add a new media type it always tends to cause a lift in reach and in sales, if the creative is working. One of the problems faced by all forms of digital is how difficult it is to get more than about a 10% reach no matter how much you spend -– the fragmentation is just so great.

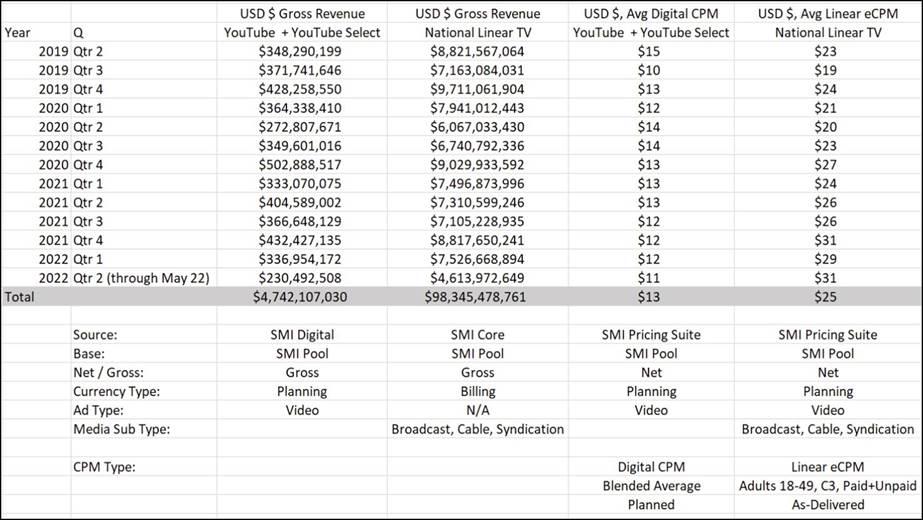

Sharing with you the latest data we have courtesy of Standard Media Index, we see that the growth of linear television and YouTube ad investments among U.S. national advertisers both hit a speed bump in Q2 as part of the general belt-tightening by marketers unsure of what the future will bring. A great opportunity for the wise to keep their ad budgets up while their competitors shrink back, and for the wise to optimize the allocation across all media types, using all of the superb tools that exist for making advertising work harder, most of which are still under-utilized.

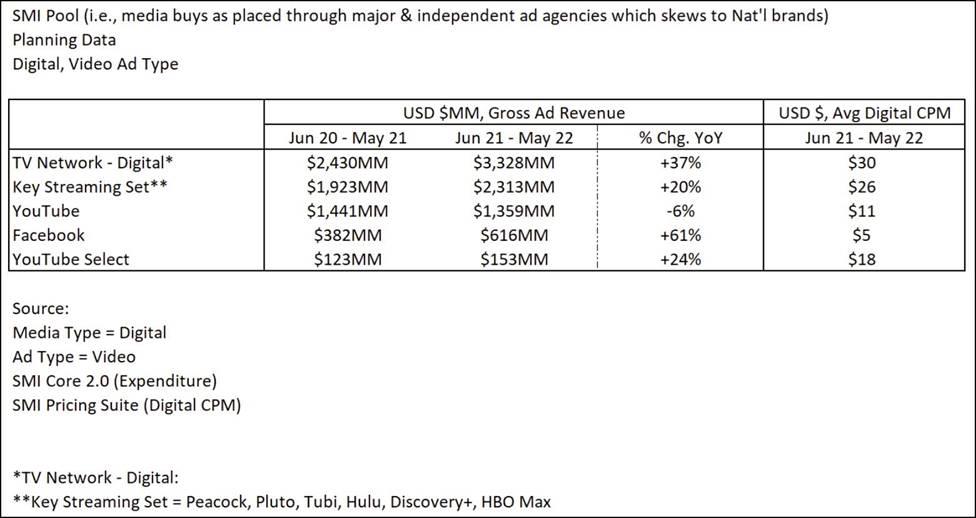

Where advertising investments are not pausing but still growing at a healthy rate is in the sphere of advertising-supported streaming type media. The digital inventory of the television networks, averaging a $30 CPM against adults 18-49 (including makegoods), is up +37% for the first five months of 2022 vs. the same period in 2021. The streaming networks spawned by the television networks are up +20% selling at a $26 CPM. Facebook digital video up +61% at $5 CPM and YouTube Select up +24% at $18 CPM, while YouTube down -6% selling at an $11 CPM.

Brands and their agencies must make use of the tools and finally make their own historic shift away from low-CPM thinking to high-ROI thinking and high-brand-equity thinking. This is not a time to cut back advertising; rather, it's time to optimize it with validated research methods. The opportunity is enlarged by streaming and all other forms of addressable TV, all forms of digital including audio and out of home, retail media, eCom, research advances, and by the shrink-back among your competitors. Now is the time to do all those visionary things you always wanted to do but no one would let you. In all this confusion you be the one who has the answers. Stand up, speak up, lead.

What are television networks to do? Although most of the decline in linear ratings is moving over into streaming, it isn’t happening 1:1. As it moves across the great divide it often winds up in a different network’s audience on the streaming side. There is no guarantee that you will catch them on the other side, and that’s where you need to focus more. On-demand AVODs and linear streaming FASTs, by being free, stand the best chance. There is still an urgent unfilled need for effective program discovery tools that transcend the obvious to provide palpable improvement in viewer experience.

Audience promotion and acquisition campaigns can be combined in purpose and targeted to exactly the right people most likely to resonate with the content of those spots. The networks in general have under-invested in audience promotion. When I first got into the business, the average new show had an awareness level of 75%. Today it has fallen below 30%. Why invest millions of dollars in developing a new series then abandon it after six weeks? It isn’t necessary to do that if you invest enough in tune-in/streaming acquisition, which budgets can be coordinated and some can do double duty.

There are new genres of television programming which you can be the one to invent. Why can’t a television network create a streaming channel for user generated content? The perfect way to finally use that next tier of talent that has been literally dying while waiting on line to get on your air for years. And to do your own talent search. And to curate content already out there that you discover and lock up first. YouTube’s 21.7% share of streaming can be shared among many competitors striving to upgrade the quality of user generated content.

As Irwin Gotlieb said, a time of confusion can be a time of opportunity.

What about the big tech companies who have come into the media business in a big way? They are all headed for the multiverse. Netflix is coming into the advertising business. Partnerships between big tech and the traditional television companies is not such a wild idea. Polarization has caused the two camps to somewhat freeze their own positions. With reality gradually settling in, more room for collaboration can be seen. Hopefully as below, so above.

Local television is an interesting wild card because of ATSC 3.0 making broadcast into digital in every way by the end of this decade. And because local TV news is as much of a cultural necessity as it has ever been. Local sports as well. The opportunity to develop original programming locally in an adaptation of user generated content might be in the cards. Already Nielsen is finding cases of half of a TV station’s audience being watched in a streaming news feed in homes that have either antenna or an MVPD they could watch it on. And stations are jumping into having their own streaming apps bigtime already.

There is a pall of feeling bad seeing the TV numbers going down. That’s not a useful feeling to have. Television is never going to go away, it’s just going to continue to morph, one set of numbers will always be going down, don’t treat it as applying to your own future in the medium. Your future is still in your hands and there are plenty of winning hands to play.

Everything up to now has just been the preview.

Click the social buttons to share this content with your friends and colleagues.

The opinions and points of view expressed in this content are exclusively the views of the author and/or subject(s) and do not necessarily represent the views of MediaVillage.com/MyersBizNet, Inc. management or associated writers.

Bill Harvey

Bill Harvey, who won an Emmy® Award in 2022 for his invention of set top box data, has spent over 35 years leading the way in media research with pioneer thinking in New Media, set top box data, optimizers, measurement standards, privacy standards, the A…