AMZN shares have outperformed GOOGL shares over the past year, and the reaction after 4Q results continued this trend. Since 1/1/17, AMZN shares are up 91% and GOOGL shares are up 41%; on Friday, after the companies reported 4Q results on Thursday after market close, AMZN shares were up 3%, adding almost $20bn in market cap, while GOOGL shares dropped 5%, chipping over $40bn from Alphabet's market cap. Bright spots in 4Q for AMZN included 1) its advertising business, contained in its other net sales and thus likely up ~60% year/year, and 2) its operating margin, reflecting upside surprise in scaling efficiencies in the holiday quarter. Operationally, the main concern for GOOGL was the continuation of the negative surprises in its operating profit margin, owing in particular to higher traffic acquisition costs (TAC) for its core advertising business.

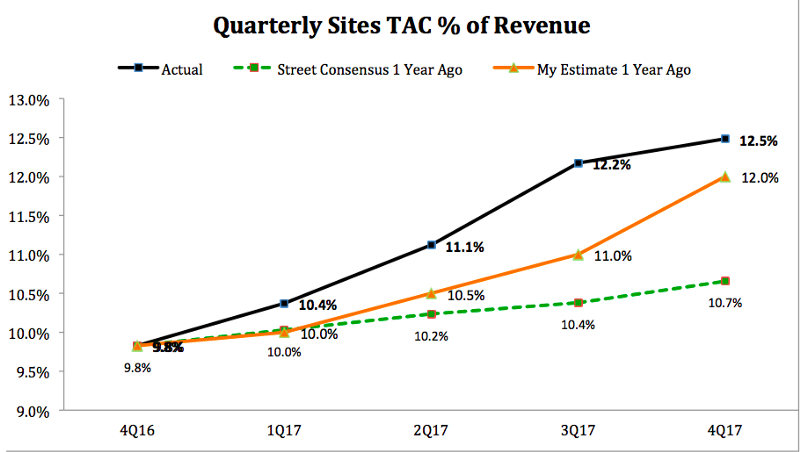

I've predicted problems for GOOGL in the past, and some have shown up and others haven't -- TAC's pressure on profitability I called right.Last February, the title of one of my reports on GOOGL said it all: "A Closer Look Reveals Sites TAC Pressures Could Be Worse Than Expected." A year ago, Wall Street expected Sites TAC % -- namely, the TAC for Google Sites (primarily Google search and YouTube) as a share of Google Sites ad revenue -- to tick up by about 1 percentage point over the course of 2017. I thought it would go up by more than twice that. The actual increase was even greater. It is valuable to look as well at the change in Sites TAC as a share of the change in revenue ("Sites new TAC %"), which measures the share of Sites revenue growth going to Sites TAC and can be a leading indicator for Sites TAC %. I expected Sites new TAC % to keep climbing in 2017, and had the 4Q17 figure about right. Wall Street actually expected Sites new TAC % to shrink in 2017.

TAC as % of GOOGL's Ad Revenue Has Been a Negative Surprise