Wall St. Speaks Out: Challenging Agency Growth Forecasts - Brian Wieser, Pivotal Research

On yesterday's earnings call with Publicis, there were some relatively contentious issues, including the company's indication that it believed the agency industry would grow by only +2.5% during 2015, down from a prior expectation of +3.0% growth.

This reduction was informed by a reduction in estimates of spending on advertising globally by the Publicis-owned media agency group ZenithOptimedia. Zenith brought expectations down from +4.9% at the time of its December forecast to +4.4% at the time of its March forecast and then to +4.2% last month. Reduced expectations are not unique to ZenithOptimedia, as Interpublic's Magna Global reduced its 2015 growth forecast from +4.8% in December to +3.9% last month.(Editor's Note: MyersBizNet forecast U.S. advertising growth earlier this year at +1.0% for 2015, and has consistently forecast more conservative growth than the agency forecasters.)

So it would seem fair to say that the consensus of two of leading forecasters of global advertising are calling for around 1% less growth now vs. the beginning of the year. In that context, if agency revenue growth were directly tied to advertising growth, Publicis' diminished expectations for the industry would be reasonable. However, most analysts were evidently struggling to connect this expectation given strong top-line organic growth results from Interpublic and Omnicom earlier in the week, and accounting for more muted expectations from WPP (which will report at the end of August).

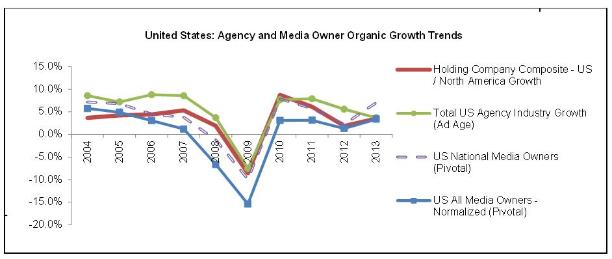

Our own take on establishing a benchmark growth rate for the industry yields a higher than Publicis' forecasts, based on our observations of historical relationships between ad spending (or media owner ad revenue) and agency revenues. To start with, we can simplify historical analysis by beginning with 2004, the year during which WPP's acquisition of Grey wrapped up the bulk of the industry's consolidation activities. We can further focus on the United States as a single market against which to compare agencies and media owners, and find the answer to be pretty straightforward.

Whether we measure agency growth by looking at the five global integrated holding companies alone or use Ad Age's annual estimates of US agency growth and compare those growth rates to media owner ad revenue growth, the agencies have been outperforming media owners and ad spending most years since 2006. 2013 was something of an anomaly, as we have noted in our recent research that advertisers increased their spending at a pace that well exceeded what should have been expected given the state of the economy at that time. Putting that year aside, agency holding company results would generally have been even higher if we excluded the Kantar research division from WPP post the TNS acquisition, and would have been higher still if we included MDC Partners (whose businesses have typically been smaller and faster growing agencies) and Aegis (which was then and is now as a part of Dentsu, primarily comprised of faster growing media and digital creative agencies).

Source: Company Reports, Pivotal Research, Ad Age

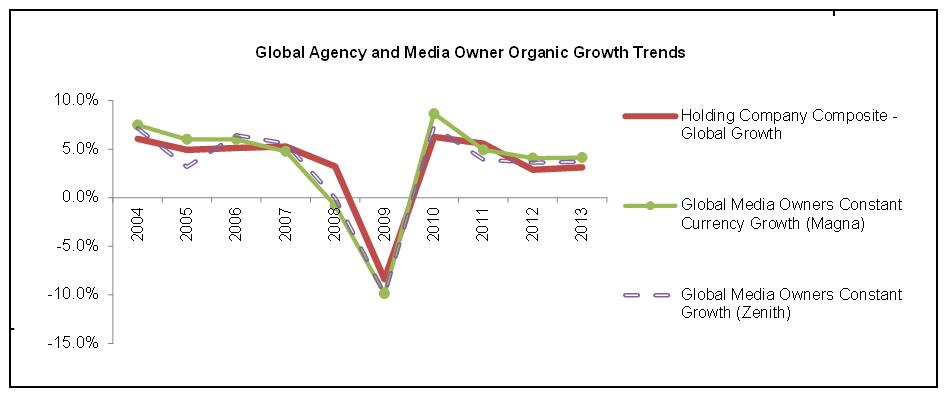

On a global level it seems that agency growth is relatively closely aligned with media owner ad revenue growth, perhaps in part because global forecasts exclude media in which agencies don't typically participate much in, such as directories). Again, the reported figures here would be slightly higher if we only looked at WPP excluding Kantar and concurrently included figures from Aegis.

Source: Company Reports, Pivotal Research, Magna Global, ZenithOptimedia

From this data, it seems that it would not be unreasonable to assume that forecasts of global media owner ad revenue growth are fair proxies for comparable figures from agency holding companies. In other words, if for 2015 Magna is at +3.9% and Zenith is at +4.2%, a 4.0% industry benchmark might be more appropriate than +2.5% in our view. Indeed, reported organic growth from Interpublic and Havas will surely exceed that level, and Omnicom probably will too.

Unfortunately, we may never again know what the "real" organic growth rate was for the industry, at least in a manner that would be historically consistent. Readers may note that the above charts abruptly end with 2013 rather than including the 2014 calendar year. This is because of the inclusion of pass-through revenues in reported organic growth from companies who do not provide a specific breakdown of net vs. gross revenue (Omnicom in particular given the inclusion of incremental "revenue" from Accuen, which the company generally discloses, and OmNet, which the company does not, as well as barter activity from Icon, which is also not disclosed). A couple of percentage points of incremental revenue from Omnicom doesn't move the needle in a meaningful way across the industry, but then again next year Publicis will incorporate activities from the newly acquired Sapient into organic growth. Presuming that Sapient returns to growth after declines during the first half of 2015, the holding company business mix will also change in a manner that renders them less comparable to the other holding companies.

2004 to 2013 might be considered golden years for benchmarking agency industry growth. For now, the relationships they describe between ad spending and agency revenue probably provide the best benchmarks we can consider for setting our expectations for industry level growth trends, although this will only be true for so long as the industry is defined as we have historically known it.

REPORT INCLUDING DISCLOSURES CAN BE FOUND HERE: Madison and Wall 7-24-15.pdf

The opinions and points of view expressed in this commentary are exclusively the views of the author and do not necessarily represent the views of MediaVillage.com management or associated bloggers.

Brian Wieser

Brian Wieser is Global President, Business Intelligence for GroupM, WPP’s media investment Group. He is leading GroupM’s thought leadership practice to ensure that WPP’s clients receive actionable marketplace intelligence on markets, audien…